A beginner-friendly guide to Social Security benefits in the USA. Learn how it works, when to claim, payment amounts, taxes, and smart strategies.

If you’re in your 50s or early 60s, Social Security benefits probably feel closer than ever.

Maybe you’ve started thinking about retirement. Maybe you’ve heard friends talk about claiming at 62. Or maybe you’re just confused about how the system really works.

You’re not alone.

For many Americans, Social Security benefits are a major source of retirement income. In fact, for some retirees, it provides half or more of their monthly income. Yet the rules can feel complicated.

This beginner-friendly guide will walk you through everything you need to know about Social Security benefits — in clear, simple language. No jargon. No confusion.

By the end, you’ll understand:

- How Social Security works

- When you can start collecting

- How much you might receive

- How to increase your benefits

- Common mistakes to avoid

Let’s start with the basics.

What Are Social Security Benefits?

Social Security benefits are monthly payments from the U.S. government to eligible workers, retirees, and certain family members.

The program is run by the Social Security Administration (SSA). It was created in 1935 to provide financial support to older Americans after retirement.

Today, Social Security benefits cover:

- Retirement benefits

- Disability benefits

- Survivor benefits

- Spousal and family benefits

Most people think only about retirement benefits, but the program is much broader.

How Social Security Works

The Basics

When you work and pay payroll taxes, you contribute to Social Security. You’ll see this deduction on your paycheck labeled “FICA.”

That money doesn’t go into a personal savings account. Instead:

- Today’s workers fund today’s retirees.

- When you retire, future workers will fund your benefits.

This system is called “pay-as-you-go.”

Earning Work Credits

To qualify for Social Security retirement benefits, you must earn work credits.

In general:

- You need 40 credits

- That usually equals about 10 years of work

You can earn up to four credits per year.

If you’ve worked full-time for at least 10 years in the United States, you likely qualify.

Types of Social Security Benefits

Understanding the different types of Social Security benefits is important, especially if you are married or widowed.

1. Retirement Benefits

This is the most common type. You can claim retirement benefits as early as age 62.

However, claiming early reduces your monthly payment permanently.

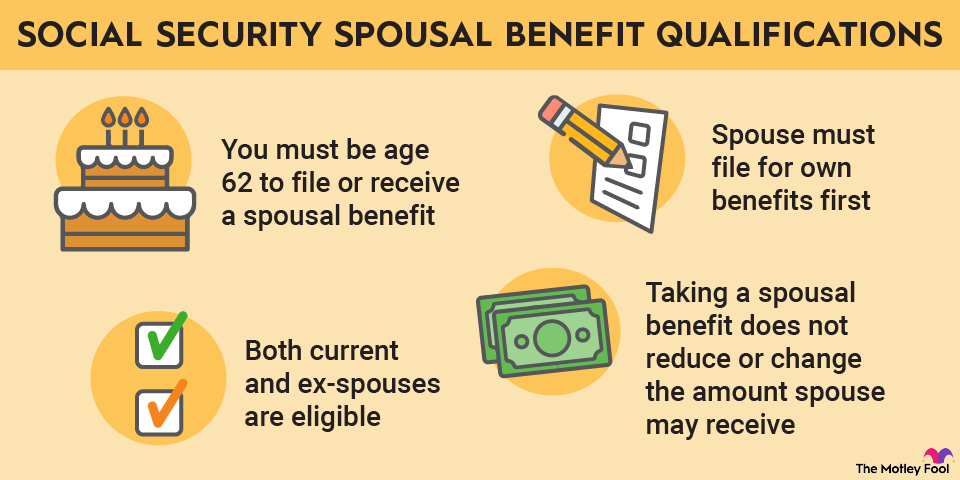

2. Spousal Benefits

If you are married, you may qualify for benefits based on your spouse’s work record.

You can receive up to 50% of your spouse’s full retirement benefit.

Even if you never worked outside the home, you may qualify.

3. Survivor Benefits

If your spouse passes away, you may receive survivor benefits.

In many cases, a surviving spouse can receive up to 100% of the deceased spouse’s benefit.

4. Disability Benefits

If you become unable to work due to a serious medical condition, you may qualify for Social Security Disability Insurance (SSDI).

This is different from retirement benefits but funded through the same system.

When Should You Claim Social Security Benefits?

This is one of the most important decisions you’ll make.

Early Retirement: Age 62

You can start collecting Social Security benefits at age 62.

But here’s the catch:

- Your benefits will be permanently reduced

- The reduction can be as much as 30%

Example:

If your full retirement benefit is $2,000 per month at age 67, claiming at 62 might reduce it to around $1,400.

That reduction lasts for life.

Full Retirement Age (FRA)

Your full retirement age depends on your birth year.

For most people born in 1960 or later, full retirement age is 67.

At this age, you receive 100% of your earned benefit.

Delaying Until Age 70

If you delay benefits beyond full retirement age, your benefit increases.

You earn about 8% more per year you delay, up to age 70.

Example:

If your benefit at 67 is $2,000:

- At 68: about $2,160

- At 69: about $2,320

- At 70: about $2,480

That increase is permanent.

For people in good health and with longer life expectancy, delaying can be a smart strategy.

How Social Security Benefits Are Calculated

Your Social Security benefits are based on:

- Your 35 highest-earning years

- Your average indexed monthly earnings

- A formula set by law

If you worked fewer than 35 years, zeros are added to the calculation.

That can reduce your benefit.

Real-Life Example

Let’s say:

- Maria worked 30 years

- She stayed home 5 years to raise children

Because she has only 30 working years, five zero-income years are included.

If she worked five additional years, her benefit would likely increase.

That’s why continuing to work longer can help boost your Social Security benefits.

How Much Will You Receive?

The amount varies greatly.

Factors include:

- Your lifetime earnings

- When you claim

- Whether you worked consistently

In recent years, the average monthly Social Security retirement benefit has been around $1,800–$2,000.

But some people receive:

- Less than $1,000

- More than $3,500

You can check your personalized estimate by creating an account at SSA.gov.

Cost-of-Living Adjustments (COLA)

Social Security benefits increase over time due to inflation.

Each year, the government may apply a Cost-of-Living Adjustment (COLA).

This helps protect retirees from rising prices for:

- Groceries

- Healthcare

- Housing

- Utilities

For seniors living on fixed income, COLA increases are important.

Are Social Security Benefits Taxable?

Yes, they can be.

If you have additional income — such as:

- Pension

- 401(k) withdrawals

- IRA income

- Rental income

You may owe federal income tax on part of your Social Security benefits.

Up to 85% of your benefit may be taxable, depending on your total income.

Some states also tax Social Security, but many do not.

This is an area where consulting a financial advisor or tax professional can help.

Working While Receiving Social Security

Many retirees continue working part-time.

If you claim before full retirement age:

- There are income limits

- Your benefits may be temporarily reduced

After full retirement age:

- There is no earnings limit

- You can work and earn as much as you want

This rule surprises many people.

If you enjoy working or need extra income, waiting until FRA gives you more flexibility.

Spousal and Divorce Rules

Even if you are divorced, you may qualify for spousal benefits if:

- The marriage lasted at least 10 years

- You are currently unmarried

- You are age 62 or older

You can claim based on your ex-spouse’s record without affecting their benefits.

This is one of the most misunderstood parts of Social Security benefits.

Social Security and Medicare

Many people enroll in Medicare at age 65.

While Social Security benefits can start at 62, Medicare eligibility begins at 65.

Even if you delay Social Security, you should still enroll in Medicare on time to avoid penalties.

Healthcare costs are one of the biggest expenses in retirement.

Understanding both programs together is important for long-term planning.

Common Mistakes to Avoid

1. Claiming Too Early Without a Plan

Many people claim at 62 simply because they can.

But if you live into your 80s or 90s, you could lose tens of thousands of dollars over time.

2. Ignoring Spousal Benefits

Couples often fail to coordinate their claiming strategy.

A smart spousal strategy can increase total household income.

3. Not Checking Your Earnings Record

Errors can happen.

Review your earnings history through your SSA account to ensure accuracy.

4. Forgetting About Taxes

Unexpected tax bills can reduce your net retirement income.

Plan ahead.

5. Not Considering Longevity

If you’re in good health and have a family history of long life, delaying may make sense.

Expert Tips to Maximize Social Security Benefits

1. Work at Least 35 Years

Avoid zero-income years in your calculation.

2. Increase Your Earnings

Higher lifetime earnings mean higher benefits.

Even a few strong earning years later in life can boost your average.

3. Delay If Possible

If financially feasible, consider delaying to age 70.

4. Coordinate With Your Spouse

Think of Social Security as a household decision, not an individual one.

5. Create a Retirement Income Plan

Combine Social Security with:

- 401(k)

- IRA

- Pension

- Savings

A financial planner can help you structure withdrawals to reduce taxes.

Real-Life Scenario: John and Linda

John is 66. Linda is 64.

John’s full retirement benefit is $2,400 at age 67.

Linda’s benefit is $1,200 at age 67.

Option 1: Claim Early

They both claim as soon as possible. Combined monthly income: lower for life.

Option 2: Delay Strategy

John delays until 70. His benefit increases significantly. Linda claims spousal benefit.

Over 20+ years, the difference could total tens of thousands of dollars.

This shows how timing matters.

How to Apply for Social Security Benefits

You can apply:

- Online

- By phone

- In person at a Social Security office

Applying online is often the easiest.

You should apply about three months before you want benefits to begin.

Have ready:

- Social Security number

- Birth certificate

- Bank account information

- Tax documents

The process usually takes a few weeks.

Planning for the Future of Social Security

You may have heard concerns about Social Security running out of money.

Current projections suggest:

- The trust fund may face shortfalls in the future

- Benefits may be reduced if Congress does not act

However, the program is unlikely to disappear.

Historically, lawmakers have made adjustments to keep it running.

For those near retirement age, major changes are less likely to affect them dramatically.

Why Social Security Benefits Matter So Much

For many retirees, Social Security is the foundation of financial security.

It helps pay for:

- Housing

- Food

- Medical care

- Utilities

Even if you have other savings, Social Security provides guaranteed lifetime income.

That reliability is powerful.

Conclusion

Understanding Social Security benefits is one of the most important steps in preparing for retirement.

The system may seem complex at first, but once you break it down, the rules become clearer.

Remember:

- Your claiming age matters

- Your earnings history matters

- Spousal strategies matter

- Taxes matter

Take time to review your personal situation.

Create a plan.

Talk with a financial professional if needed.

Most importantly, make an informed decision — not a rushed one.

Your future self will thank you.

Frequently Asked Questions (FAQs)

1. What is the best age to claim Social Security benefits?

The best age depends on your health, income needs, and life expectancy. Claiming at 62 gives you money sooner but reduces your monthly benefit permanently. Waiting until full retirement age gives you 100% of your earned benefit. Delaying until age 70 increases your benefit by about 8% per year. If you expect to live a long life and can afford to wait, delaying may provide higher lifetime income.

2. How are Social Security benefits calculated for beginners?

Social Security benefits are calculated using your 35 highest-earning years. The government adjusts your earnings for inflation and averages them. If you worked fewer than 35 years, zeros are included in the formula. The result determines your monthly benefit at full retirement age. Claiming earlier reduces it, and delaying increases it.

3. Can I work while collecting Social Security benefits?

Yes, you can work while receiving benefits. If you claim before full retirement age, there is an earnings limit, and benefits may be temporarily reduced. Once you reach full retirement age, you can earn unlimited income without reductions. Working longer may also increase future benefits if your earnings replace lower-income years.

4. Are Social Security benefits enough to live on in retirement?

For some retirees, Social Security benefits cover basic living expenses. However, for many Americans, it replaces only about 40% of pre-retirement income. Most experts recommend additional savings such as a 401(k), IRA, or pension. Social Security should be viewed as a foundation, not the entire retirement plan.

5. Are Social Security benefits taxable in retirement?

Yes, Social Security benefits can be taxable depending on your total income. If you have other income sources like pensions or retirement withdrawals, up to 85% of your benefit may be subject to federal income tax. Some states also tax benefits. Planning withdrawals carefully can reduce tax impact.

6. What happens to Social Security benefits if my spouse dies?

If your spouse dies, you may qualify for survivor benefits. In many cases, you can receive up to 100% of your spouse’s benefit if it is higher than yours. Survivor rules depend on age and other factors. It’s important to contact the Social Security Administration after a spouse’s passing.

7. Can divorced individuals receive Social Security benefits?

Yes, if you were married for at least 10 years and are currently unmarried, you may qualify for benefits based on your ex-spouse’s record. You must be at least 62 years old. Claiming on an ex-spouse’s record does not reduce their benefit.

8. How do cost-of-living adjustments affect Social Security benefits?

Cost-of-Living Adjustments (COLA) are annual increases based on inflation. They help Social Security benefits keep up with rising prices. When inflation increases, your monthly payment may increase as well. This helps protect retirees from losing purchasing power over time.

9. What is the difference between Social Security and Medicare?

Social Security provides income during retirement, while Medicare provides health insurance starting at age 65. You can claim Social Security as early as 62, but Medicare eligibility begins at 65. Even if you delay Social Security, you should enroll in Medicare on time to avoid penalties.

10. How do I check my estimated Social Security benefits online?

You can create an account at the official Social Security Administration website to view your earnings history and estimated benefits. This tool allows you to see projections based on different claiming ages. Reviewing your estimate regularly helps you plan better for retirement.